How Microfinance Empowers Women in Developing Countries: A Path to Mental Freedom and Financial Independence

“Introduction to Microfinance: Meaning, Importance, and Role in Financial Inclusion”

Microfinance is a powerful tool that provides small loans, savings, and financial services to individuals who are traditionally excluded from the formal banking system. It primarily supports low-income families, women, and small entrepreneurs, helping them break the cycle of poverty and achieve financial independence. Unlike conventional banks that require collateral, microfinance institutions (MFIs) focus on trust, community participation, and repayment through small installments.

The concept of microfinance gained global recognition through the efforts of Dr. Muhammad Yunus and the Grameen Bank in Bangladesh. Today, it has expanded worldwide, playing a crucial role in promoting financial inclusion and sustainable development. Microfinance not only offers credit but also encourages savings, micro-insurance, and skill development, empowering people to build small businesses, improve education, and enhance healthcare.

One of the key benefits of microfinance is women empowerment. By giving women access to financial resources, microfinance helps them contribute to household income, make independent decisions, and uplift their families. Women empowerment also fosters entrepreneurship, enabling women to start small ventures and achieve self-reliance. In rural and urban areas alike, microfinance creates opportunities for women empowerment that strengthen communities. Ultimately, women empowerment through microfinance leads to long-term social and economic transformation.

“The Role of Microfinance in Women’s Empowerment and Mental Freedom”

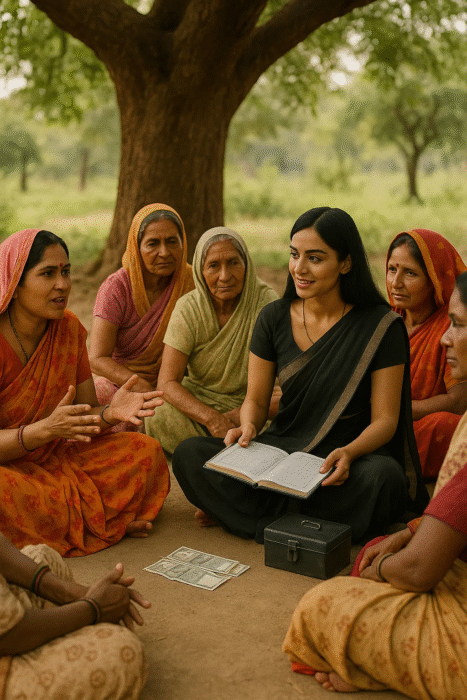

In a remote village, a Rs. 500 loan didn’t just buy sewing supplies—it bought dignity, voice, and mental freedom for a woman who had never owned anything before. That small amount of money allowed her to start a micro-business, contribute to her household, and, most importantly, feel seen and heard in ways she never had before.

This is the silent revolution of microfinance. While it might look like just a transaction on paper, for millions of women across developing countries, it represents a doorway to autonomy, self-worth, and resilience. True women empowerment begins when financial access meets self-awareness and opportunity.

Microfinance—providing small loans and financial services to people traditionally excluded from banking—has become one of the most powerful catalysts for change. It’s not just about lending money; it’s about lending confidence, trust, and a chance to rewrite one’s story.

The impact goes far beyond financial independence. When women gain the ability to make decisions about money, they also gain a sense of mental clarity and self-determination. Suddenly, how Money Matters become Mind Matters in the journey toward a Happy Life becomes evident.

This blog explores how microfinance programs empower women not only economically but emotionally, mentally, and socially. From breaking the cycle of poverty to reducing stress and fostering optimism, microfinance has proven to be more than a financial tool—it is a movement toward true personal growth and community transformation.

When were Small Finance Banks introduced in India?

The concept of Small Finance Banks (SFBs) in India was formally introduced by the Reserve Bank of India (RBI) in 2014, with the aim of deepening financial inclusion. The RBI issued guidelines to create a new category of banks that could cater to the unbanked and underbanked segments of society—primarily small businesses, marginal farmers, micro and small industries, and low-income households.

History of Small Finance Banks in India

The idea emerged from the need to bring microfinance institutions (MFIs), local area banks, and other community-based financial entities under a structured and regulated framework. By granting them a banking license, the RBI ensured they could mobilize deposits, provide small loans, and operate within a more secure environment.

In September 2015, the RBI granted in-principle approval to 10 entities, including Ujjivan, Equitas, Janalakshmi, and AU Financiers, to set up Small Finance Banks. Most of these institutions had a strong presence in microfinance, which made the transition smoother. By 2016–2017, the first wave of SFBs began operations.

Objectives of Small Finance Banks

The primary objectives behind introducing Small Finance Banks were:

- To promote financial inclusion by offering savings, deposits, and loans to those outside the formal banking system.

- To serve the needs of rural and semi-urban populations, especially women, farmers, and small entrepreneurs.

- To formalize microfinance lending practices and bring them under regulatory oversight.

Role of Small Finance Banks in Financial Inclusion

Since their introduction, SFBs have played a crucial role in transforming access to credit. Unlike traditional commercial banks, they focus on small-ticket loans, doorstep banking, and personalized customer service. Many of these banks also run financial literacy programs, ensuring that clients—especially women—gain confidence in handling money.

Small Finance Banks and Women Empowerment

Research shows that when women access microfinance or banking services, household decision-making power improves. SFBs, much like microfinance institutions, target women borrowers for group loans or micro-enterprise funding. This not only reduces default risks but also strengthens social capital, giving women greater dignity and independence.

“The Microfinance Revolution: Empowering Women Beyond Money”

Banking the Unbanked: A Tool for Dignity

- Statistical Insight: According to the World Bank, nearly 80% of microfinance clients globally are women. This statistic isn’t coincidental—it highlights the transformative potential women carry when provided with financial access.

- Beyond Transactions: Microfinance often works through group lending models, where women form circles of trust. This creates not just accountability but also social capital—a safety net of encouragement and support.

- Case Study: The Grameen Bank in Bangladesh pioneered this model. Research shows women who participated weren’t just paying back loans; they were also gaining decision-making power within their households. For many, it was the first time their voices were heard in family or village matters.

Microfinance here is not charity. It is empowerment through trust, responsibility, and opportunity.

The Mental Freedom Dividend

From Survival Mindset to Possibility Thinking

- Psychological Shift: Women who once worried daily about food or rent now begin to dream about expansion, education for their children, or even savings. With economic agency comes a reduction in chronic stress and anxiety.

- The Confidence Loop: Success breeds confidence. When women successfully run a small shop or tailoring business, they gain self-worth. This self-worth then fuels bigger ambitions, creating a virtuous cycle of growth.

- Research Spotlight: Studies reveal that microfinance participants report higher life satisfaction and optimism, with significant reductions in mental distress compared to non-participants.

This is the mental freedom dividend—the priceless shift from survival mode to possibility thinking.

Mind Matters: The Cognitive Transformation

How Financial Literacy Rewires Neural Pathways

- Numerical Empowerment: In many cultures, women are discouraged from handling money. Microfinance programs not only break this taboo but give women practical skills like budgeting and saving.

- Decision-Making Muscles: At first, women make small daily choices—what to buy, how to price goods. Over time, these grow into strategic decisions like expanding businesses or reinvesting profits.

- The Planning Horizon: Perhaps the most profound change is learning to think in the future tense—to plan months or years ahead, something poverty often robs people of.

Microfinance thus doesn’t just shift bank balances—it reshapes thought patterns.

Health for Women: The Embodied Impact

When Income Meets Wellness

One of the most powerful outcomes of microfinance is its direct link to women’s health and overall well-being. With increased income, women can finally afford to bring nutrient-rich foods into their homes instead of relying solely on low-cost staples. This shift in diet improves not only their health but also the growth and immunity of their children. Access to healthcare also expands—prenatal checkups, vaccinations, and menstrual health products become within reach, leading to healthier families and stronger communities. Moreover, financial security reduces constant stress. Women sleep better, worry less about emergencies, and gain the mental space to focus on growth. Ultimately, the body reflects this transformation, mirroring the freedom and dignity that financial independence brings.

The Positive Mindset Ecosystem

How Microfinance Creates Optimism Networks

Microfinance is more than just a financial tool—it is a catalyst for building optimism and resilience within communities. One of the most powerful aspects lies in its group dynamics. Lending circles not only provide women with access to capital but also create safe spaces for sharing challenges and brainstorming solutions. This collective approach strengthens women empowerment by reducing isolation and building mutual trust. Through collaboration, women empowerment turns financial assistance into lasting confidence and courage.

Another crucial outcome is success modeling. When women witness their peers succeed—whether by expanding a small business, sending their children to school, or purchasing a new asset—it sparks belief. This visibility reinforces women empowerment, showing that success is achievable and within reach. The ripple effect of inspiration nurtures women empowerment, motivating others to dream bigger, work harder, and pursue independence with determination.

The benefits extend even further through intergenerational impact. Daughters of microfinance clients are more likely to attend school, aspire for higher education, and break cycles of dependency. Such changes demonstrate the depth of women empowerment, shaping futures through education and opportunity. Sons, too, grow up witnessing their mothers’ strength, further promoting women empowerment and challenging traditional gender roles in society.

In essence, microfinance does not just empower an individual woman; it uplifts entire ecosystems. It builds networks of optimism, resilience, and hope—laying the foundation for happier families and stronger communities. At its core, women empowerment becomes the driver of community transformation and progress. By multiplying opportunities, women empowerment ensures that growth is sustainable, inclusive, and shared across generations.

Implementing Effective Microfinance Programs: Beyond Money for Women Empowerment

Successful microfinance programs go far beyond simply disbursing small loans. To truly empower women and create lasting transformation, these initiatives must integrate education, technology, and cultural understanding. Effective microfinance works best when women not only gain access to capital but also the skills and support needed to maximize its impact.

Financial Literacy Training: Providing training on budgeting, saving, and debt management ensures that women can manage their loans effectively. When women understand how to track income and expenses, they gain control over their financial future and can build sustainable businesses.

Mobile Banking Access: Digital tools and mobile banking platforms break barriers for women, especially in rural or remote areas. Mobile transactions reduce dependency on intermediaries, increase security, and allow women to save and transfer money with ease.

Cultural Sensitivity: Programs designed with local traditions, values, and gender dynamics in mind have higher success rates. Respecting cultural nuances helps in building trust and ensures women feel included, safe, and supported.

Ultimately, effective microfinance programs are not one-size-fits-all. Their true strength lies in adapting to local realities while empowering women with knowledge, access, and dignity. When implemented thoughtfully, microfinance becomes a powerful catalyst for gender equality, community growth, and a pathway to a happy life.

Conclusion: The Ripple Effect of Empowerment

Microfinance proves that even the smallest loans can create massive ripple effects. At its core, microfinance is more than a financial transaction—it is a catalyst for long-term change. When these tools are designed with women in mind, they do more than address economic needs. They open doors to personal growth, mental freedom, and opportunities for leadership that women may never have imagined possible.

For many women, a loan of just Rs. 500 is not merely capital. It becomes a symbol of confidence, dignity, and hope. It represents the trust placed in them and the belief that they, too, can shape their destiny. With access to such resources, women are able to invest in small businesses, secure their children’s education, and ensure better healthcare for their families. The ripple effect continues, as empowered women often reinvest their earnings back into their households and communities, creating a cycle of prosperity.

The true beauty of microfinance lies in its ability to uplift entire communities through individual empowerment. Each story of transformation becomes a beacon of inspiration for others, proving that change is possible even with limited means.

Call to Action:

- Support organizations that champion women empowerment through ethical microfinance programs.

- Share stories of women who have transformed their families and communities through small loans.

- Download our free guide to gender-lens investing and learn how you can play an active role in this global movement.

Because when women rise, communities flourish—and the journey to a Happy Life often begins with just one empowered step.

Leave a Reply